OCBC 360 vs DBS Multiplier vs UOB one

The top 3 banks in Singapore are offering attractive saving accounts for you to park their money at their bank.

DBS - DBS Multiplier programme

OCBC - OCBC 360 account

If you are a conservative spender like me who doesn't earn a lot, let see which account offers the best deal

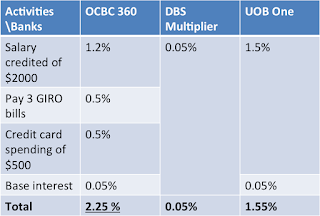

Case 1:

Assuming salary credited of $2000

Credit card spending = $500

OCBC 360 wins in this case, paying the most interest of 2.25%.

Case 2:

OCBC 360 wins in this case, paying the most interest of 1.25%.

UOB wins in this case, paying the most interest of 1.05%.

DBS - DBS Multiplier programme

OCBC - OCBC 360 account

UOB - UOB One account

If you are a conservative spender like me who doesn't earn a lot, let see which account offers the best deal

Case 1:

Assuming salary credited of $2000

Credit card spending = $500

OCBC 360 wins in this case, paying the most interest of 2.25%.

Case 2:

Assuming salary credited of $2000

Refused to own credit cards, credit card spending = $0

Case 3:

Salary less than $2000/salary not GIRO into bank

Credit card spending = $500

UOB wins in this case, paying the most interest of 1.05%.

Depending on your income and monthly expenditures, different bank accounts will suit different people. DBS multiplier will suit the heavy investor, with interest of 2.08% if the Salary+ credit card spending + Home loan instalments + investment dividends amounts to $20,000 and above.

UOB will suit one who has salary <$2000/ Salary not paid by GIRO, but has credit card spending of >$500.

For OCBC 360, it will pay 1.2% if salary > $2000 is credited even if we do not do anything.

For me, it is bye DBS, hello OCBC :)

It’s interesting to see how each account shines under different spending and salary crediting scenarios and how OCBC 360 often comes out strong for everyday savers. I’d love to see a follow-up that also touches on how linked products like home loans can factor in overall banking value, especially when comparing offers like the DBS home loan rate alongside savings account perks.

ReplyDelete